Authors

What’s Next for the Credit Cycle?

Key Takeaways

- We believe the credit cycle will remain in the expansion phase, despite a number of macroeconomic headwinds. We expect solid growth supported by healthy risk appetite, strong corporate health, easy financial conditions and fiscal policy.

- The war in the Middle East has a wide range of potential outcomes. However, the US economy entered the conflict with a broadly supportive economic, monetary and fiscal backdrop, and we believe it will remain resilient through the volatility. If oil prices surge toward $150/barrel and are sustained for a prolonged period, then economic risks would rise, in our view.

- We expect energy prices to add inflationary pressure, but we don’t anticipate a period of sustained wage/price inflation because the labor market is soft. Recall that even with some tariff-induced inflation in 2025, the US saw continued disinflation that allowed the Federal Reserve (Fed) to cut interest rates.

- Despite cooling labor market data, we are not expecting a massive wave in layoffs. We view corporate health as the linchpin behind the labor market, and corporate earnings have been strong.

- Energy-induced inflation has many central banks (and the markets) rethinking the path of policy rates. The new Fed Chair incoming in May 2026 will likely have to walk a tightrope with a soft labor market and energy-induced inflation picking up, in our view.

Graphic Source: Loomis Sayles. Views as of March 26, 2026. The graphic presented is shown for illustrative purposes only. Some or all of the information on this chart may be dated, and, therefore, should not be the basis to purchase or sell any securities. Any opinions or forecasts contained herein reflect the current subjective judgments and assumptions of the authors only, and do not necessarily reflect the views of Loomis, Sayles & Company, L.P. This information is subject to change at any time without notice.

Expansionary Dynamics

We expect solid GDP growth of approximately 2% throughout 2026. We believe a positive fiscal impulse, lower policy rates, supportive financial conditions and continued strength in earnings sets the stage for healthy growth conditions despite the disruption from the war in the Middle East.

The Trump administration seems determined to uphold tariff policy through new avenues. There are still question marks surrounding potential refunds of tariffs implemented via the International Emergency Economic Powers Act. If refunds are paid out to US businesses, they could provide additional stimulus, but the process will likely be messy and slow. The impact of tariffs on inflation has been less aggressive than initially expected, but now there’s energy-induced inflation to contend with. However, we don’t anticipate a period of sustained wage/price inflation because the labor market is soft. We believe US inflation will drift gradually down to the Fed’s 2% target once the energy-induced spike in headline inflation subsides, though that process could take months.

We could see some continued friction in the labor market, but we do not expect a massive wave in layoffs in the near-to-medium term as long as corporate health remains solid. Corporate earnings have been strong. Our most recent survey of Loomis Sayles’ credit analysts (our Credit Analyst Diffusion Indices, or CANDIs), conducted in January, showed improving expectations for profit margins and leverage. The Loomis Sayles Credit Health Index (CHIN) is currently well above typical expansion/late cycle levels.

We believe profits are one of the most important indicators to watch because they drive the cycle. If declining demand or increased costs hit margins and profits turn negative, then companies are more likely to start shedding labor. As long as profits remain broad-based and positive, we anticipate a fairly “Goldilocks” environment for risk assets, with some pockets of volatility.

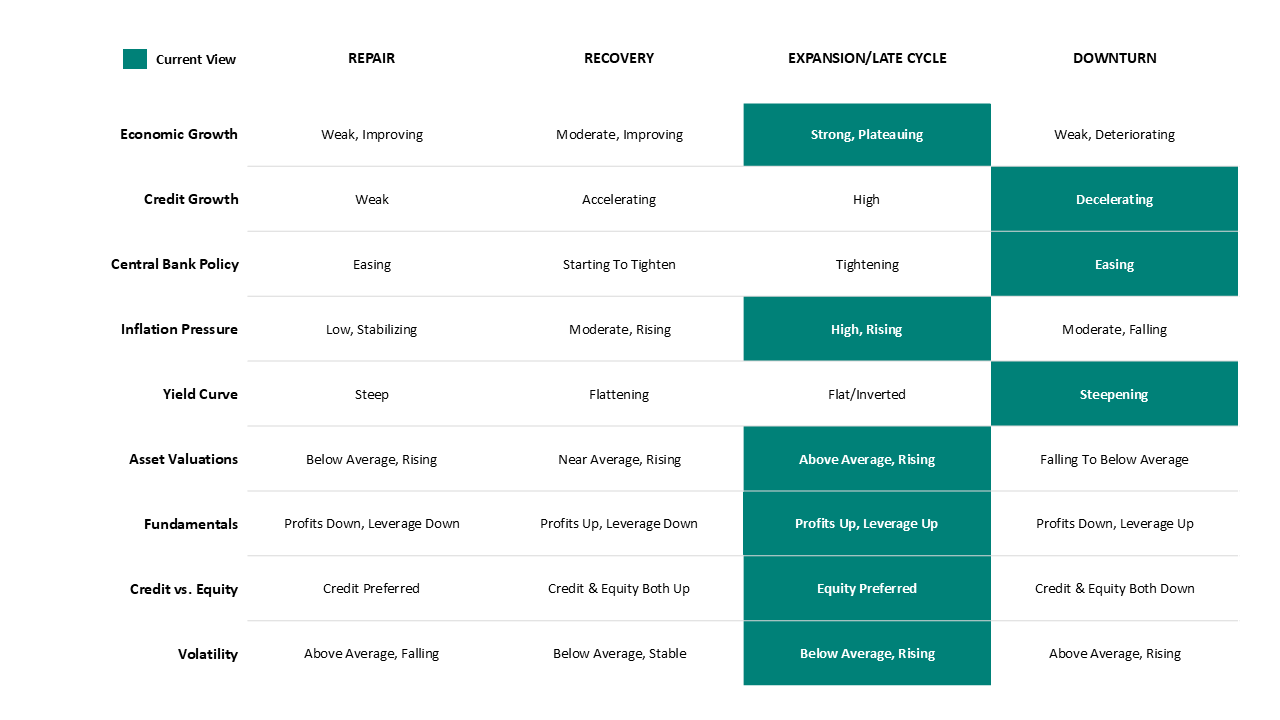

A Closer Look

In our view, credit cycle analysis requires art and science. We track key economic indicators that tend to behave differently in each phase of the cycle, and put them into context using our credit cycle framework and collective experience. Currently, these indicators primarily fall within expansion/late cycle. We believe the credit cycle remains in this phase of the cycle based largely on the strength of bottom-up fundamentals. At this stage of the cycle, investors tend to focus on capital preservation and moving up in quality.

Table Source: Loomis Sayles. Views as of March 26, 2026. Highlighted cells represent attributes we’re currently observing. Green represents our current view. The table presented is shown for illustrative purposes only. Some or all of the information on this chart may be dated, and therefore, should not be the basis to purchase or sell any securities.

What’s Next?

Because macroeconomic factors don’t always behave as expected, we prepare scenarios for the path of the US credit cycle over the next six months. Here are three potential scenarios and indicators to watch:

Base Case

Expansion/Resilient

- In this scenario, strong corporate health, consumer spending and fiscal policy drive the economy and support solid growth.

- The war in the Middle East evolves into a persistent but lower-intensity conflict with an anticipated negotiated settlement. Oil prices remain elevated due to restricted oil supplies. Markets may react to newsflow, but the overall impact on the credit cycle remains contained.

- The labor market may cool with softer supply and early signs of weakening demand, but strong corporate profits help limit large-scale layoffs.

- Inflation gradually trends downward with soft goods inflation, lower shelter inflation and more limited wage pressure.

- The Fed waits for energy prices to level off before interest rate cuts continue.

Alternative Scenario

Late Cycle/Economic Boom

- This scenario recognizes further upside for the US economy, fueled by the potential for a higher fiscal multiplier, elevated capital expenditures and/or strong consumer spending among higher-income consumers.

- The war in the Middle East is quickly resolved and energy prices drop toward pre-conflict levels in the $60-$70/barrel range.

- Profits remain elevated, unemployment is low and inflation remains sticky near 3% given the strong demand backdrop.

- The Fed takes a more cautious stance and pauses interest rate cuts.

- Risk assets rally given the strong macroeconomic backdrop, though rising yields could spark market volatility.

Alternative Scenario

Downturn

- In this scenario, labor market friction turns into more significant disruption. Companies shed labor to save costs as the profit outlook worsens in the face of rising energy costs.

- The war in the Middle East escalates into a major, prolonged conflict with oil being sustained in the $120-150/barrel range for many months.

- A sustained correction in the equity market diminishes the wealth effect, hitting the higher-income consumers that have been supporting aggregate consumer spending, and consumption rolls over.

- The Fed cuts interest rates, yields rally and risk assets sell off.

Macro Themes in a Flash

Our views on key topics that can influence the credit cycle.

Middle East War/Oil

Our view: We entered the conflict with a broadly supportive economic backdrop. We would need to see persistently high oil prices to increase our odds of a downturn materially.

The details: There are a wide range of potential outcomes in this war. We think the most likely scenario is a persistent, low-intensity conflict that could last months. In our view, oil prices are likely to range between $85-$100 in the near term, with occasional spikes higher. Markets are likely to react to newsflow, but we believe the overall impact on the credit cycle will be contained thanks to a solid macroeconomic backdrop and corporate health.

The US Consumer

Our view: The consumer still appears fairly healthy in aggregate.

The details: Higher- and lower-income consumers have been spending at healthy levels.i Elevated tax refunds this year should help support consumption. We’ll be watching the wealth effect closely—it has been a large factor propping up spending over the past few years.

Global Growth

Our view: Global economies are typically more exposed to large energy shocks compared to the US. We would expect the global economy to slow marginally given the rise in energy costs, but we are not expecting a recessionary environment. Global growth was looking more synchronized coming into 2026, supported by interest rate cuts in 2025. Countries have the ability to increase fiscal spending to support their economies if needed.

The details: In our view, the risk of a sustained rise in energy prices causing a widespread recession is a tail risk for now. We have seen stronger manufacturing PMI data, which suggests some positive cyclical momentum for the global economy. China is exiting deflation. Europe appears to be in the early stages of the credit cycle, driven by interest rate cuts, improving financial conditions and substantial and iterative fiscal stimulus. External risks remain relevant on a global scale, especially with elevated geopolitical tension, but there is more resilience globally compared to the energy shock that followed the beginning of the Russia/Ukraine war.ii

US Monetary Policy

Our view: We think the Fed will resume cutting interest rates but the timing is more uncertain. We had anticipated a couple of “fine-tuning” interest rate cuts by the summer of 2026, but now we think those cuts may be pushed out to late 2026. A lot hinges on the soft labor market balanced with the potential for energy prices to pass through to goods inflation.

The details: We think a softer labor market and a resumption of disinflation should pave the way for additional interest rate cuts by the end of the year. New Fed leadership may push for an easier bias, looking to take a forward view on potential productivity, but it’s unclear if the Federal Open Market Committee would be on board with that stance. For the Fed to cut 100 basis points or more, we believe it would likely want to see accelerating disinflation and weaker non-farm payrolls data.

US Corporate Profits

Our view: Corporate earnings growth has been very strong, handily beating expectations. We expect equity earnings-per-share (EPS) growth to remain solid through 2026, though consensus forecasts already appear bullish.

The details: We believe earnings growth can broaden out this year, and large-cap earnings could potentially achieve double-digit growth rates.

US Credit Risk Premium/Risk Appetite

Our view: Credit spreads were very tight at the start of 2026, but widened marginally since early March. Wider spreads seem more associated with the increased risk of downgrades and defaults stemming from software/AI disruption than the threats from the war in the Middle East. Given how solid corporate fundamentals have been, we think a widening of credit spreads would present a more compelling opportunity to add credit risk compared to what was on offer in 2025.

The details: Credit fundamentals still look solid and the technical backdrop has helped keep spreads contained. Compressed credit spreads have led us to look for value in other segments of the fixed income markets, such as mortgage-backed securities and other securitized debts. We would view further corporate credit spread widening as an opportunity because all-in yield remains attractive and aggregate credit fundamentals still look relatively healthy.

Inflation

Our view: We expect US inflation to drift gradually down to the Fed’s 2% target, though the energy-induced spike in headline inflation may delay that process until the back half of the year.

The details: We expect inflation to taper off and hit the Fed’s target in 2027 as energy costs and tariffs fade into the background. Businesses appear to be passing along tariff hikes gradually. Goods inflation pressure has subsided, shelter inflation should continue to cool and wage pressure has softened.iii

Artificial Intelligence (AI)

Our view: AI spending can help support the economy. We think it is likely to drive further productivity gains, though the process will be somewhat gradual and uneven. AI is still in its early innings.

The details: The global economy has seen some productivity gains (even without the introduction of AI) after a very weak period following the Great Financial Crisis. We expect productivity gains to continue, though the magnitude and timing are uncertain. Labor market disruptions have been mostly concentrated thus far; we don’t anticipate significant near-term displacement under our base case scenario. Capital expenditures have been immense and are expected to continue. AI spending has been largely funded by cash flows so far, but we are seeing increased debt issuance. Most hyperscalers are healthy, profitable companies, in our view.iv

The US Dollar

Our view: We believe the potential for a US dollar bull market remains low, especially if the Fed cuts interest rates later this year while other central banks hold or tighten policy.

The details: The US dollar tends to trade with a firm tone when international developments pose risk to overall financial market stability. We still believe non-US-dollar assets can perform well as the expansion progresses, but ongoing Middle East conflict has lowered our optimism and expectations. When global growth expectations begin to stabilize or even improve, a more bullish stance for owning non-US-dollar assets will return quickly, in our view.

China

Our view: Inflation in China appears to be moving out of negative territory after three years of deep deflation.

The details: We believe higher inflation in China could serve as a catalyst for broader economic improvement. The People’s Bank of China is likely to continue easing with small and gradual interest rate cuts. We think the temporary US-China tariff truce will hold, and we anticipate non-US demand to support China’s trade surplus in 2026. Overall, we anticipate real GDP growth of approximately 4.5%-5.0% in 2026.

Endnotes

i Based on data from Bank of America, through February 2026.

ii PMI data from S&P Global, as of February 2026. China deflation data from China’s National Bureau of Statistics, as of February 2026.

iii Inflation data from the US Bureau of Labor Statistics, through February 2026. Wage data from the Federal Reserve Bank of Atlanta wage growth tracker, through February 2026.

iv Productivity and labor market data from the Bureau of Labor Statistics, through Q4 2025 and February 2026, respectively. Capital expenditures as indicated by individual company Q4 2025 balance sheets. Bloomberg consensus expectations as of March 24, 2026. AI spending funded via cash flows from the Federal Reserve Board, as of Q4 2025. Debt issuance data from Bloomberg, as of March 24, 2026.

Disclosure

All insights and views are as of March 25, 2026, unless otherwise noted.

This marketing communication is provided for informational purposes only and should not be construed as investment advice. Any opinions or forecasts contained herein, reflect the subjective judgments and assumptions of the authors only, and do not necessarily reflect the views of Loomis, Sayles & Company, L.P. Investment recommendations may be inconsistent with these opinions. There is no assurance that developments will transpire as forecasted and actual results will be different. Data and analysis does not represent the actual, or expected future performance of any investment product. Information, including that obtained from outside sources, is believed to be correct, but Loomis Sayles cannot guarantee its accuracy. This information is subject to change at any time without notice.

Indices are unmanaged and do not incur fees. It is not possible to invest directly in an index.

Commodity, interest and derivative trading involve substantial risk of loss.

Any investment that has the possibility for profits also has the possibility of losses, including the loss of principal.

Markets are extremely fluid and change frequently.

Past market experience is no guarantee of future results.

8210502.1.4

Meet the Authors